Want to learn more? The Hutchins Center and Center on Health Policy will convene a meeting on May 2 to explore policies that can help rein in prescription drug prices. Register for the webcast or to attend in person.

Americans spend a lot on prescription drugs, more per capita than any other country by far. Pharmaceuticals represent a significant—and growing—share of the country’s health spending, both because new, and often costly, drugs are emerging from the lab and because prices of many drugs are rising much faster than prices of other goods and services. The Center for Medicare and Medicaid Services (CMS) estimates prescription drug spending will grow an average of 6.3% per year over the 2016-2025 period. Highly publicized cases of very expensive new drugs as well as sharp increases in the price of some older drugs has drawn widespread attention—and criticism—from the public, members of Congress and President Donald Trump. Because the U.S. government pays more than 40% of the retail prescription drug tab, rising spending on drugs is putting pressure on the federal budget. It also contributes to rising health insurance premiums.

In this explainer, we describe recent trends in drug spending, what’s driving them, and what role government policy plays.

How much does the U.S. spend on prescription drugs?

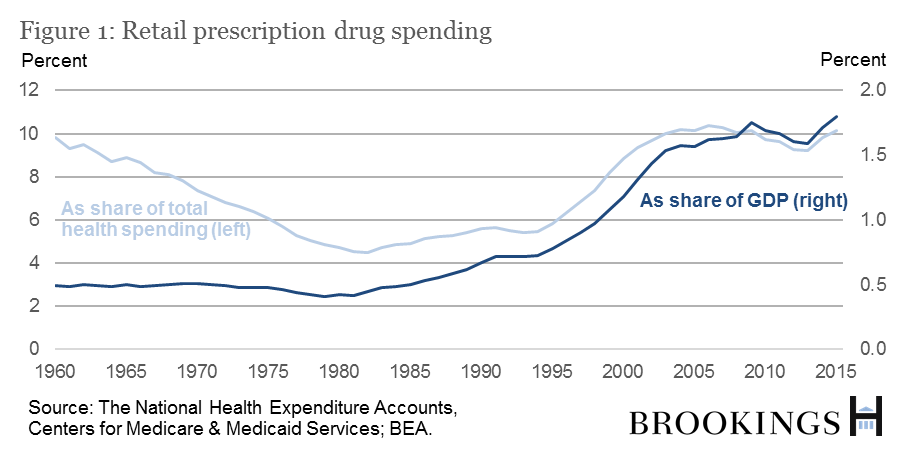

In 2015, the U.S. spent $325 billion on retail prescription drugs (drugs purchased at pharmacies and through the mail, as opposed to those administered directly by doctors), according to the Centers for Medicare & Medicaid Services. That’s 1.8% of GDP, or 10% of total national health expenditures.

How has U.S. retail prescription drug spending changed over time?

It has grown considerably since the 1980s. Figure 1 shows retail prescription drug spending since 1960, both as a share of GDP and as a share of total health spending. It rose from the early 1980s to the early 2000s (by both measures), and then after a period of slow growth, rose sharply in 2014 and 2015.

Note that all of the above statistics are “net” of rebates and discounts, which is important, because drug manufacturers make heavy use of rebates and discounts to boost demand. Many news articles and pundits focus on list prices, making overall spending look larger than it is in reality.

Why did retail prescription drug spending go up in 2014 and 2015 after so many years of small increases?

There appear to be several factors. One is that fewer major patents expired in 2014 and 2015, and when a patent expires and generic drugs enter the market, prices drop. According to IMS Health, in 2012 and 2013, 14 brands (including Plavix and Lexapro) experienced $500 million or more in lost revenue due to new generic competition, but in 2014 and 2015 that was only true for nine brands (including Nexium and Lunesta).

Another is that several high-priced blockbuster hepatitis C drugs (Harvoni, Sovaldi, etc.) reached the market with sales in 2014 and 2015 equal to about 40 percent of the net increase in US spending on prescription drugs. Expensive new treatments for multiple sclerosis, diabetes, and cancer also were introduced.

How does U.S. spending on pharmaceuticals compare to that of other countries?

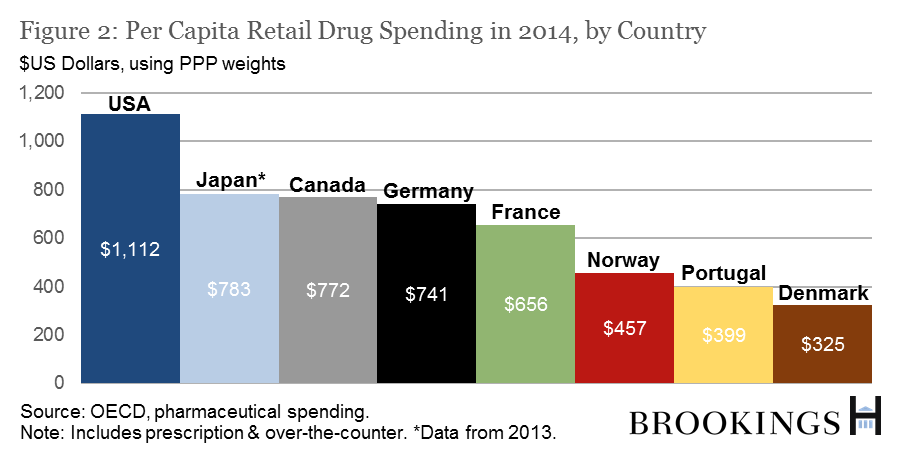

The U.S. spends substantially more per capita than other countries. According to the OECD, the U.S. spent $1,112 on retail pharmaceuticals per person in 2014 (including over-the-counter purchases). The next highest spender was Canada, at $772, followed by Germany at $741 and France at $659. 2014 data is not yet available for Japan, but in 2013, its per person expenditure was $782. Some advanced economies spending considerably less were Norway ($457), Portugal ($399), and Denmark ($325).

Who foots the bill?

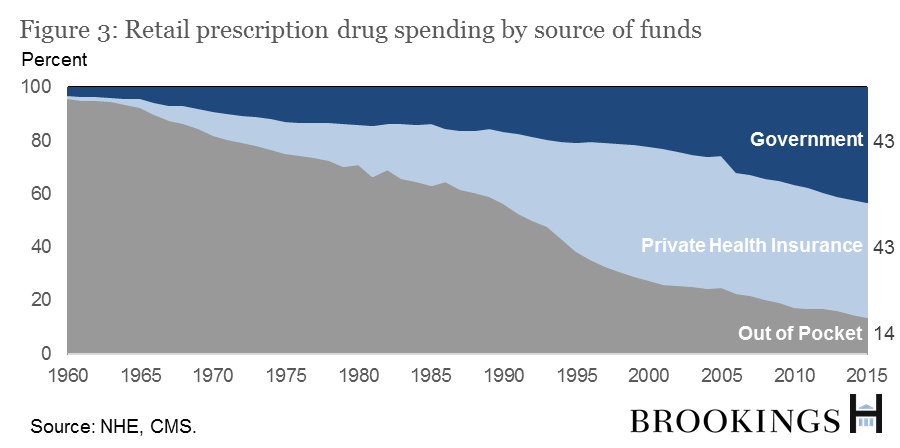

In 2015, the US government paid roughly 43% of all retail prescription drug costs—29% through Medicare, 10% through Medicaid, and the rest through the Department of Defense, the Department of Veterans Affairs, Children’s Health Insurance Program (CHIP), and some smaller federal and state programs. (See Figure 3.) The share of the bill paid out of pocket by consumers has been dropping since 1960, and is now around 14%, and the share paid by private health insurers has been stable at about 40% for the past 10 or so years—in 2015, it made up 43% of total retail prescription drug costs.

Figure 3 shows a jump in the government’s overall share of retail prescription drug costs in 2006 when Medicare Part D, which provides subsidized prescription drugs for the elderly, took effect. Before the introduction of Part D, Medicare covered prescription drugs administered in hospitals and some other settings through Part A and Part B, but not retail prescription drugs. Medicare Part D provided subsidies for seniors wishing to purchase prescription drug insurance, and as of year-end 2015, 35 million senior citizens were using it.

This large, rising government share gives the government a strong interest in determining whether its purchases of new high-priced brand-name drugs in 2014 and 2015 represented money well spent, or whether pharmaceutical companies have undue pricing power.

If the government is such a significant buyer in the prescription drug market, can it negotiate lower drug prices?

For the most part, no. When Congress created Medicare Part D, it prohibited Medicare from negotiating with drug companies for lower drug prices. Congress also required eligible Medicare Part D plans to offer coverage for essentially all drugs in certain disease categories. Drug companies still face price pressure on drugs in the non-protected classes, though, because the private insurers that offer plans through Medicare Part D are able to negotiate.

The situation for Medicaid—the federal-state health insurance program for low-income Americans—is different. The Federal government doesn’t negotiate Medicaid prices directly (though states can). Instead, by law it sets drug prices at the lowest amount others are paying, or sometimes even lower.

The exception is the U.S. Department of Veterans Affairs (VA), which negotiates prices outright and is able to exclude drugs from coverage, but accounts for only a small share of overall government drug spending.

Why does the government permit temporary monopolies through patents and the FDA’s market exclusivity arrangements? What is the effect?

The government is balancing two competing factors: It wants to give pharmaceutical companies financial incentives to innovate and produce breakthrough drugs, but it also wants to keep drug prices as low as possible. These are often in tension. If the government lets drug companies charge hundreds of thousands of dollars to develop a life-saving cancer treatment, more companies will be willing to take the risks inherent in such an uncertain research project. But if the government lets drug companies do that, annual costs will rise, particularly because very sick people might be willing to pay arbitrarily high prices for life-saving remedies. Finding an appropriate balance is difficult.

Related Books

The current system for incentivizing drug research works as follows: The normal 20-year patent term (most drugs are covered by several) applies to drugs from the time of the patent, usually before clinical tries are conducted. In addition, the Food and Drug Administration (FDA) can grant temporary market exclusivity rights, which guarantee that the FDA will not approve a generic competitor for a set period of time.

These two forms of protection from competition—exclusivity from the FDA, and patents—interact in complicated ways, but the result is that on average, brand-name drugs have 13 or so years of sales before a generic competitor enters the market.

Is qualifying for “orphan status” one way a drug can get exclusivity from the FDA?

Yes. If a drug shows it treats a rare disease, it can get orphan drug status and seven years of exclusivity—an incentive established by the Orphan Drug Act of 1983 to encourage more drug companies to treat neglected populations. According to the FDA, it has worked: Drug companies have created hundreds of rare-disease drugs since 1983, compared to 10 in the decade prior.

But some are concerned the designation is being abused by companies who come up with clever ways to get their existing drugs to qualify, repeatedly, for its benefits. NPR reports “about a third of orphan approvals by the FDA since the program began have been either for repurposed mass market drugs or drugs that received multiple orphan approvals.”

When patents and exclusivity run out and generics enter the market, how much do they lower drug spending?

A lot. According to researchers at Duke University and Analysis Group, within one year of the entrance of a generic competitor, brand-name drugs first experiencing generic competition in 2011-2012 went from having 100% market share to 11% on average. They also note that “generic products’ share of total prescriptions in the US increased from 36% in 1994 to 84% in 2012.”

Why has the market share of generic drugs grown so quickly over the past few decades?

The Duke and Analysis Group researchers identify three causes. The first is the Hatch-Waxman Act of 1984, which (1) incentivized generic drug companies to challenge brand-name drug patents, and (2) allowed generic drug companies to show that their drugs were equivalent to brand-name drugs before getting approval instead of requiring them to conduct a battery of expensive clinical trials.

The second is that insurers began actively promoting generics by letting patients pay smaller co-pays for them than for brand-name drugs, and in some cases by not covering brand-name drugs if generics were available.

The third is that many states passed laws allowing “generic forms to be substituted automatically by pharmacists for brand-name drugs prescribed by physicians, so long as physicians have not specified that the prescription must be ‘dispensed as written’” (emphasis added).

What about spending on non-retail prescription drugs?

It is much harder to track non-retail prescription drugs (drugs administered directly by physicians in hospitals and doctors’ offices) than it is to track retail. The Altarum Institute calculates that non-retail prescription expenditures make up about 30% of total prescription drug spending.

What can the U.S. do to slow the rise in prescription drug prices without discouraging innovation?

Some believe that the system isn’t broken—that overall life expectancy has increased over the past few decades in part due to prescription drug innovations, and the costs are worth the benefits. Others think that the government should take radical steps, such as funding all drug research and development and doing away with the patent system. Still, others believe the system should be modified, but not completely overhauled.

Authors

Commentary

The Hutchins Center Explains: Prescription drug spending

April 26, 2017